It’s easy to feel bearish in the current environment. Just read almost any news headline or check your investment accounts.

The negativity hits on a short ride around town. For example, I swear our local gas prices rose a dime during my 15-minute round trip to the grocery store this weekend. Of course, gas prices notoriously influence sentiment because they’re so prominent. But, for many, the psychological pain far outweighs the relatively affordable higher cost.

We’re so susceptible to avoiding losses that we’re constantly doing the worst things, usually also at the worst time. Fear clouds our judgment. As a result, we often sell at the bottom when the pain is most intense.

We also miss out on buying opportunities that require decisive, contrarian action.

You’re likely familiar with these traditional behavioral weaknesses, but I’m increasingly concerned about a counterintuitive twist: bad news making people too bullish.

Let’s call this group complacent contrarians.

Their thought process goes like this: “Sure, things are bad, but smart investors like me love to buy on weakness. In any case, I’m a long-term investor.” Maybe you know someone like this.

This insidious complacency prevents these investors from noticing when important facts have changed. Instead, their success in an irrelevant past anchors their approach in unhelpful ways. As a result, these overconfident investors roll out the same old playbook just as market prices scream to confirm a significant pattern shift.

For years, buying volatility on weakness in a stable regime worked pretty well.

It can be dangerous for those wired this way to stay bullish in a falling market. And that’s where the catastrophic damage occurs.

What’s needed instead is sober reflection and flexibility.

The world of multifamily has its share of complacent contrarians too. They talk about inflation protection, housing shortages, and double-digit rent increases. And as the operating and financing environment gets more challenging, many sponsors effectively roll out the same playbook.

They show their compelling track records and offer the same pro forma returns they’ve promised and exceeded over the past decade. Rarely questioned is whether the past decade is at all relevant.

The feedback mechanism in private markets is slower, and therefore trend shifts need more time to emerge. That ambiguity is a function of liquidity, turnover, and price transparency. So at potential turning points, a bit more prudence is warranted.

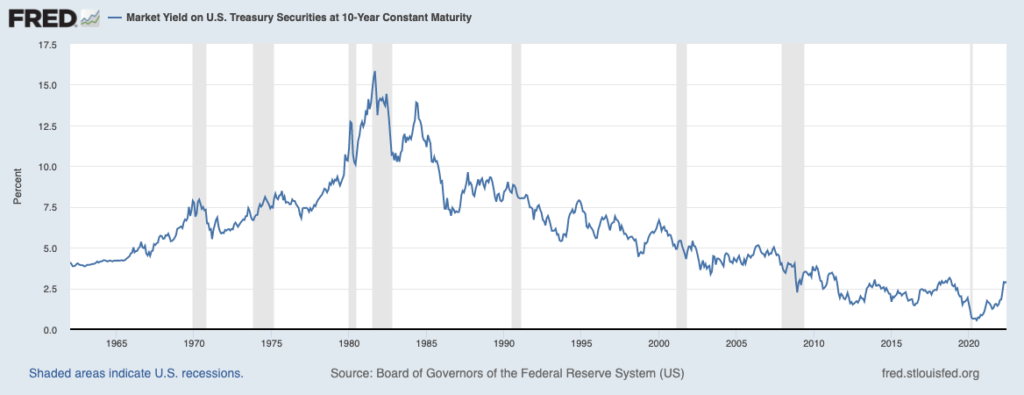

Remember that real estate is a leveraged asset that does well when interest rates decline. Investors have enjoyed a tremendous macro tailwind at our backs for 40 years. Falling interest rates (not to mention an accommodative Fed) have bailed out a lot of bad investments and made a lot of people feel and look pretty smart. I’ve had my share of lucky breaks along the way.

Have we conclusively entered a new macro regime marked by persistently higher inflation? I have no idea. But I think this question warrants serious consideration. Because if we have, you might want a different portfolio and investment strategy than what’s worked over the past 40 years.

Without a functioning crystal ball, I don’t have answers. But I think we can start with some good questions.

How about, “How will you adapt if the tailwind we’ve enjoyed for 40 years becomes a headwind?” That seems like a good place to begin the conversation.