Here we go. Fancy new title. Broader mandate. Yet somehow, I can’t move forward without first sharing some thoughts on multifamily real estate valuations. Mainly, that’s because I don’t get it.

Please note that nothing I write should ever be considered investment advice. The current investing environment must be one of the most difficult in decades.

The following comments represent my current gut reaction to the current pricing environment for multifamily assets. Over the coming weeks, I plan to update this view by adding rigor (more analysis, references, and charts) and subtracting fluff. At that point, I hope to have more conviction on the medium and long-term outlook than I do today. But unfortunately, I’m not there today.

Writing anchors and challenges my thought process, and you should expect my views to evolve. I welcome your input and feedback.

My TLDR: I think the fundamental outlook remains strong overall, but it seems reasonable to expect some valuation adjustments in the short term.

In the context of the general macro backdrop (rising rates and bond yields, inflation, and slowing growth), I understand most of the recent global market action. But one anomaly stands out. Private market valuations for apartments strike me as oddly inconsistent with the rest of the landscape.

Consider the following (as of 5/20/22):

- S&P 500 YTD total return: -17.7%

- Nasdaq Composite YTD total return: -27.4%

- Increase in US 10 Year Treasury Yield YTD: +126bps, 1.52% on 12/31 to 2.78% on 12/20

- Bitcoin YTD Return: -36%

- REZ (ETF tracking publicly traded resi REITs) YTD return: -15.7%

- Cap rates (income yields) for private market MF deals: unchanged

If a publicly-traded stock with lower leverage is down 20%, how much should a less liquid, less diversified, more highly leveraged vehicle be down? Like most things, it depends, but it’s hard to argue that it’s zero.

That doesn’t seem conservative to me. Yet that’s what we’re still seeing in private market transactions.

Remember that data for private transactions is less transparent than more liquid public markets. From my conversations with brokers, I can tell you that cap rates haven’t yet budged.

Competition for apartment deals remains intense at record low cap rates (income yields) despite rapidly rising mortgage rates, lower loan proceeds (leverage) offered by lenders, much higher costs to cap variable-rate loans, and headwinds from operating cost inflation.

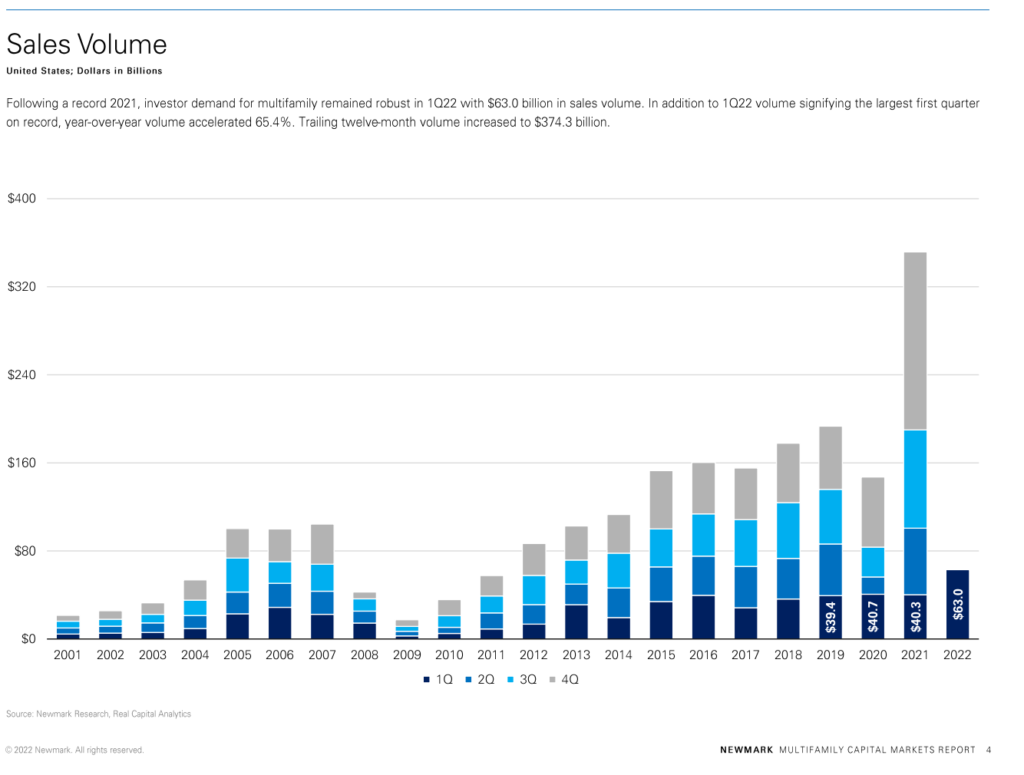

Yet investors can’t seem to get enough. According to Newmark, Q1 sales volumes were the highest on record.

At a minimum, the same deal with lower leverage implies lower returns to equity, all else equal. Usually, prices would adjust to reflect that. However, since we assume that trailing NOI wouldn’t change, trailing cap rates would have to rise. This adjustment hasn’t happened. Yet.

Sophisticated investors price assets on sober estimates of future rental income and operating expenses. While fundamentals are still strong, it’s hard to ignore that the macro backdrop has materially changed. At a minimum, the risk of change is higher than we’ve seen in years. More risk typically expresses itself in the form of a discount to compensate the buyer for that higher risk. Something has to give.

Berkadia is one of the largest commercial lenders in the country. Their latest market commentary indicates that things may be shifting.

“However, there has yet to be a material change in pricing or cap rates, but Berkadia continues to watch this closely as the market is constantly changing. Based on conversations and observations, the private leveraged buyer appears to be experiencing more challenges and are less competitive in today’s marketplace because they are unable to obtain full loan proceeds. As a result, there have been fewer private capital investors submitting competitive offers. On the flip side, the institutional investor is sitting in a more competitive position today given their cost of capital and ability to execute, but they have become more discriminating on the deals they pursue.”

Berkadia market Commentary – 5.11.22

Am I Bearish?

Not really. Take my comments above at face value. It’s oddly inconsistent that there’s been no price adjustment yet, but that doesn’t mean I’m bearish either. The structural outlook remains solid.

What would make me more bearish? Oversupply (especially at lower costs), significant and negative changes in government policy, or higher real rates. For now, I don’t see any of these factors in place. That said, the latest housing initiative from the White House warrants closer analysis. Through several coordinated programs, the goal is to increase access to affordable housing by substantially boosting the supply. It is an open question whether the country can deliver on its goals without further increasing construction costs.

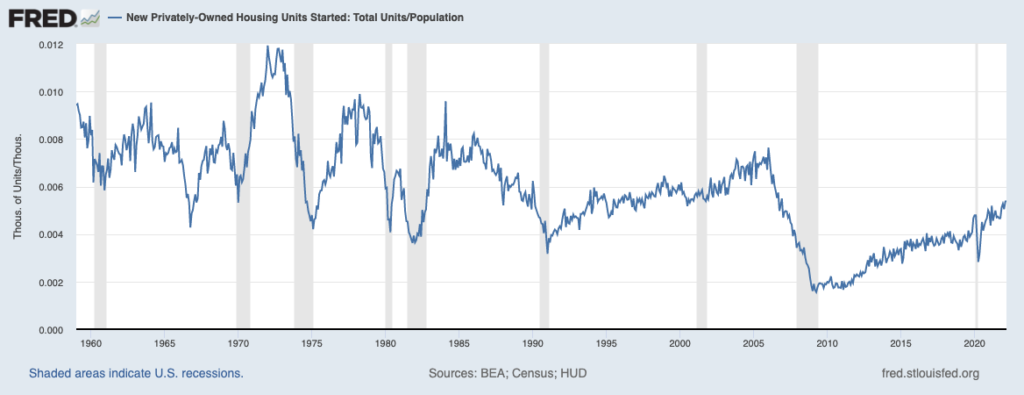

For now, vacancy is extraordinarily tight. While supply additions are high relative to the past decade, we’re hardly making a dent in the chronic undersupply of housing that should prevent any significant supply disruption. Moreover, when adjusted for population, we’re only approaching the lower bound of what had been the normal range of construction for roughly 50 years.

And keep in mind that all of this new construction is coming in online at a higher cost and will likely face delays associated with ongoing shortages of labor and materials.

I do worry about the outlook for rent growth for properties serving residents with lower incomes where affordability is already stretched to the limits.

The 2022 America’s Rental Housing Report from the Joint Center for Housing Studies at Harvard reminds us that fully 36% of renter households make less than $30,000 per year. The traditional Class B/C value-add playbook in which you renovate and bump rents by $100-$200/month could be testing its limits. At this stage of the cycle, how many of the residents remaining in our low-cost rental stock can afford those renovated units. The risk here is that the market can’t support the pro forma rent growth assumptions or that we see much higher delinquencies and costly evictions.

I’m still looking for good deals. If the numbers work, then we’ll share opportunities with investors. I’m hopeful but also skeptical that we’ll find much soon. I guess the risk is that we miss out. I’ve never been comfortable investing if success required an anomaly to persist. If I miss out on a heated market getting hotter, I’m ok with that.

I think it’s appropriate to be compensated at least somewhat for the significant risks currently affecting the rest of the universe. Cap Rates were 100bps higher only a year ago and were more than 200bps higher the last time the 10yr was above 3% (the mid-2010s).

A 100-200bps move higher may not be the right target. But I don’t think 0bps higher seems appropriate either.

I may be wrong. The apartment market may stand firm, and prices may even accelerate higher as disappointed capital from stocks and crypto chase the relative stability of housing.

It wouldn’t be that interesting if it were obvious. So let’s see how this plays out.