In our recent post, “Fears of An Apartment Exodus” we shared our views around the significant shortage of affordable housing in this country and why it’s unlikely that “everyone” will leave their apartments in the city for a single-family home in the suburbs. Supply constraints make an apartment exodus impossible in practice – we can’t push a button and automatically have millions of new homes – it also ignores the issue of affordability when demand exceeds supply. Millions of apartment residents would probably move to a home today, either to rent or to buy, if they could afford it. The reality is that they cannot. And as demand increases, we see prices in suburban markets rising, moving further out of reach for many would-be buyers. Therefore there is a segment of the rental market called “renter by necessity,” a population that lives in Class B and C apartment buildings.

The longer-term demand trends workforce and/or affordable housing remains solid. And for reasons discussed in our prior post, the supply situation still looks manageable outside of the high-end Class A space in key markets (not our focus).

As with any investment, there’s always something to worry about. There’s no free lunch. So what do we worry about and more importantly, what can we do about it?

Below we share our thoughts on the following: Execution, Market Oversupply, Cap Rates, Economic Weakness and Tax Law Changes.

The Biggest Risk: Execution

If we’ve underwritten a deal appropriately, purchased the property at a reasonable price, used conservative leverage, then the most significant risk is execution. The basics matter. A lot. We’re talking about marketing to drive traffic, leasing vacant units, collecting rent, responding to maintenance calls from residents, overseeing renovations.

For this reason, we work with experienced, professional property management companies in our local markets, who have operated through multiple economic cycles. We have standing calls with these on-site teams to address potential issues early and make changes as needed.

Maybe we don’t “worry” about execution because it’s such a core area of focus. Obsessive attention to operations and the right partners on the ground can significantly reduce our risk.

Market Oversupply

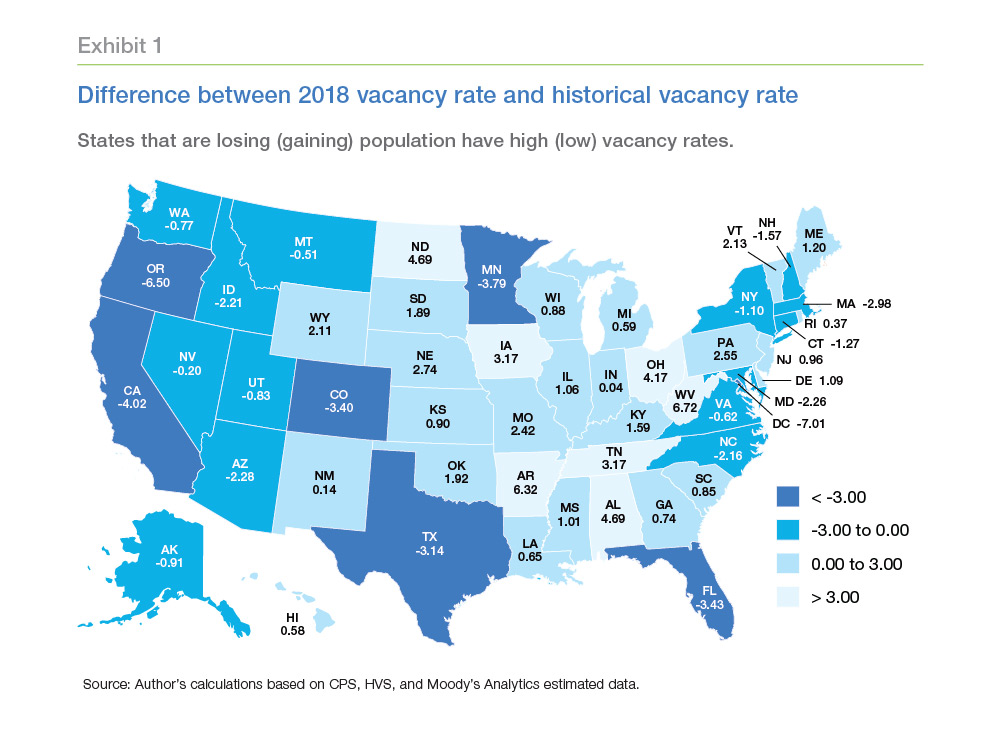

Real Estate remains a capital intensive business that is inherently cyclical. When returns are good, the asset class will attract capital, which will ultimately depress future returns. It’s normal to expect overshooting on the upside and the downside since information is imperfect and new projects reflect significant upfront costs. What may seen to be an appropriate level of supply can problematic if demand rapidly shifts across local markets.

Acknowledging this uncertainty, we do our best to minimize our exposure to oversupply. One way we do this is to focus on growing markets. Once built, apartment buildings of 125-250 units will be in place for 40-50 years or more. Without demand growth, it’s difficult for supply to adjust. A growing market can absorb temporary oversupply within a reasonable period.

For reasons discussed in our prior post, we don’t believe that our segment of the apartment market, Class B/C faces a significant risk of oversupply at the national level. Clearly, specific local markets will better be positioned than others. We cannot predict whether other developers will choose to add significant capacity to a local market, but we can select markets that will be affected less impacted if they do.

For more on this topic examining trends at the state level, see Freddie Mac’s Research note, “The Housing Supply Shortage: The State of the States.”

Cap Rates

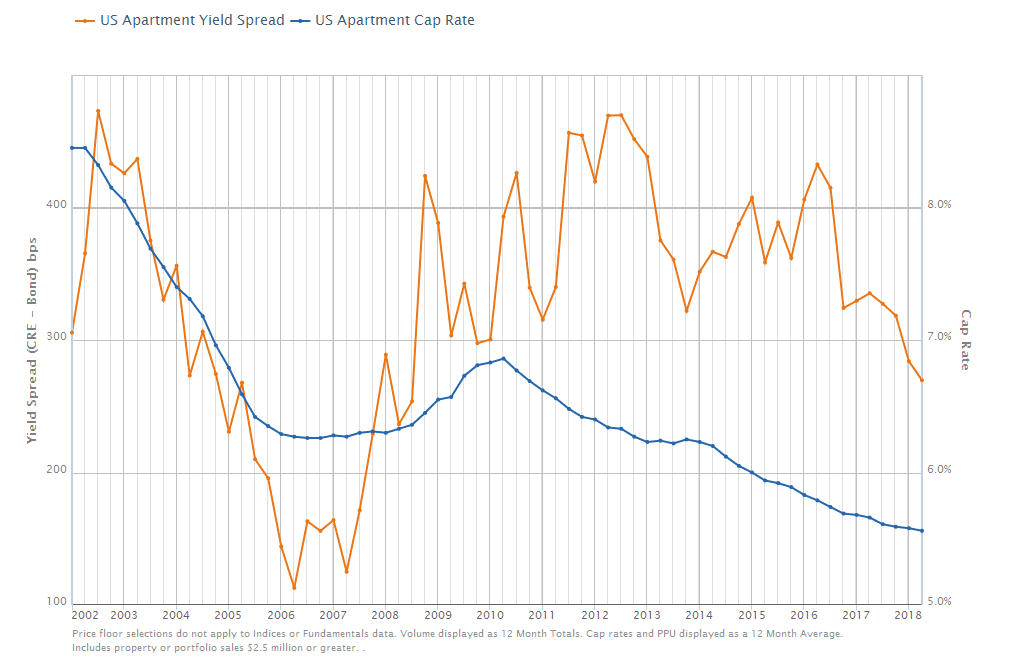

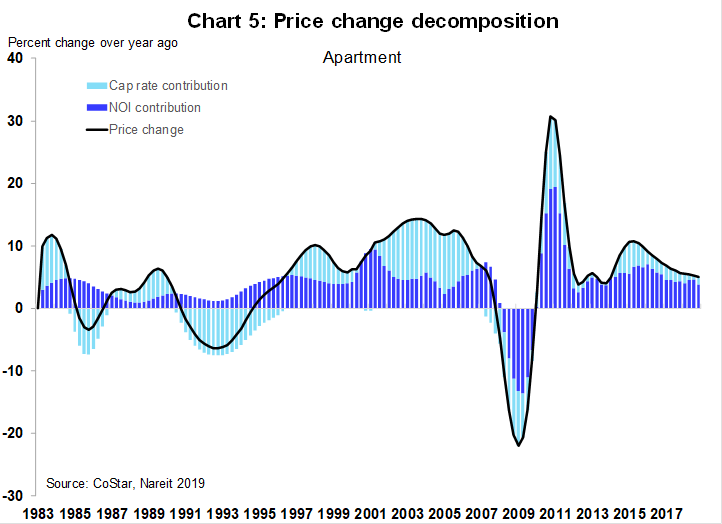

Capitalization Rates, or “Cap Rates,” are nothing more than the normalized net operating income of a property divided by the price of the property. What it tells us is how much investors are willing to pay for a given property’s cash flow, which incorporates investors’ views of the local market and their expectation of future cash flow. The other factor at play is the general level of market interest rates for other cash flow streams, like bonds. Over the long-term, cap rates have tended to trend with a spread to real bond yields.

We will not claim to have any insight into the direction of real bond yields. For years we’ve grappled with ever lower rates, and many countries have even seen their nominal government bond yields turn negative. In June of 2019 we discussed this topic in our blog post called Global Influences on Local Investments. More than a year later, we still have no strong conviction into the future direction of interest rates.

So how do we mitigate the risk of rapidly rising bond yields and cap rates that will, all else being equal, depress the value of our real estate when it comes time to exit? The primary strategy here is to focus on increasing the normalized NOI through some form of renovation. A value-add component to an investment can enable the operators to raise rents, which will drive higher NOI. This is called forced-appreciation in real estate parlance.

Depending on the drivers of higher interest rates beyond the scope of this article, value-add strategies may not fully offset higher cap rates. In allocating capital it’s important to consider alternatives. It’s likely that rising rates will impact bond prices and especially longer duration assets like equities. It’s possible that outside of cash, apartments may prove to be somewhat resilient in such a rate-driven downturn.

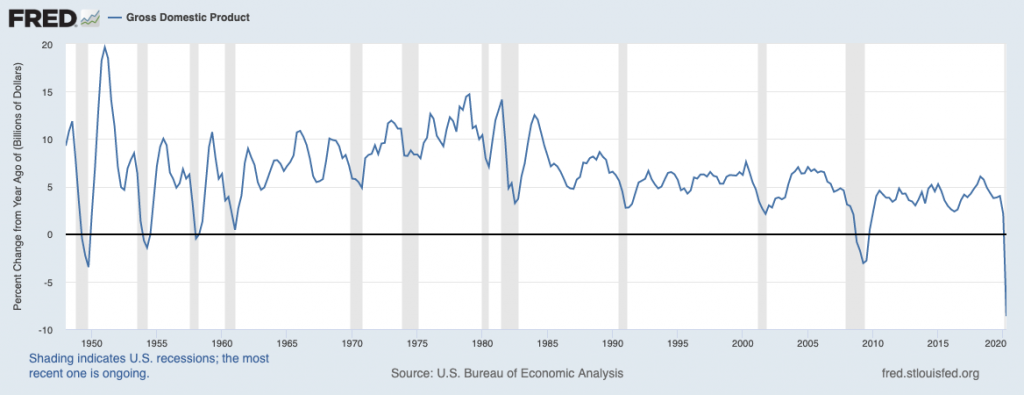

Economic Weakness

A slowdown in the economy, defined as a recession, has tended to happen every 4-5 years on average. Therefore, any investor considering a 5-7 year holding period in an apartment building should expect at least one period of weakness to occur. Of course, the frequency, magnitude, and composition of these downturns vary. So while we don’t know what the next recession will look like, we know it’s always around the corner.

Because we expect periods of higher vacancy and lower rents, we prepare in advance so that we can ride out the more difficult times. Specifically, it’s critical to have sufficient reserves available to fund operating and interest expenses. If your underwriting is too aggressive, or if you haven’t built your reserves, it may be too late when the recession hits.

It’s also worth noting that by focusing on more affordable segments of the market, we’ll normally see a “trade-down” affect where Class A residents will seek less expensive rent to reduce costs. At $700-$900 per unit for an average 1 bedroom across our portfolio, we’re often one of the more affordable options in our markets, even if a resident is temporarily relying on unemployment benefits.

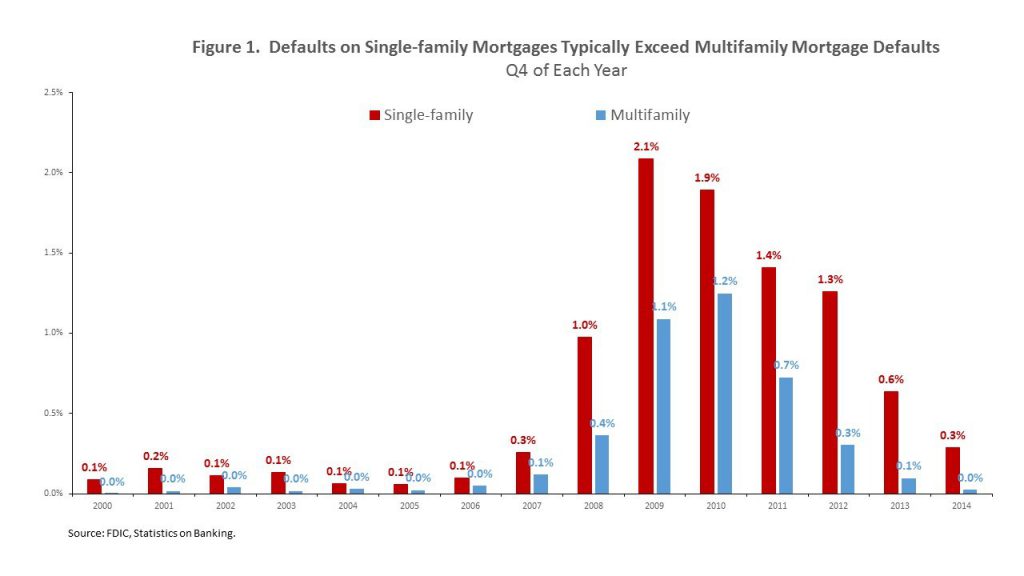

Defaults in the multifamily sector have historically been manageable, even during the Great Financial Crisis, largely due to the relative stability of rental income, even in a downturn. Having a diversification benefit of many residents instead of a single-family explain must of this effect.

Tax Law Changes

This is the one area that concerns us the most because there isn’t anything that can be done to manage our exposure. For decades, real estate has enjoyed very friendly tax treatment. We believe that it’s good tax policy to incentivize investment where it’s needed for the benefit of society. As we’ve highlighted, the US faces a serious affordable housing shortage. We also believe that political leaders appreciate the important role that private investors play in addressing this issue.

Still, anything can happen. Laws can change. It’s possible that we see some adjustments to regulatory policy or even a reversal of recent tax benefits from the 2017 Tax Law. Or even a higher capital gains tax rate for all asset classes. We don’t believe marginal changes would significantly disrupt the investment outlook for apartment buildings relative to other options.

What would really concern us is a major reversal in the long-standing policy allowing the deductibility of real estate depreciation to offset income. This is one of the more attractive benefits of investing in real estate. And while a reversal of this benefit would adversely affect the value of real estate investments and reduce the incentive to build and improve real estate assets in the US, changes are always a possibility. It only takes a vote by Congress and there are many precedents of radical changes to tax policy.

To conclude, we’ve highlighted some of the key risks that we monitor as real estate investors. This is not meant to be an exhaustive list, but we do hope it provides some insight into our framework for evaluating and mitigating these potential risks.