Given the dramatic move we’ve seen in interest rates in recent weeks, I thought it was important to revisit some of my own assumptions around how my chosen strategy, value-add multifamily real estate, might be affected. There’s no better way for me to organize my thoughts than through writing and sharing, so here goes.

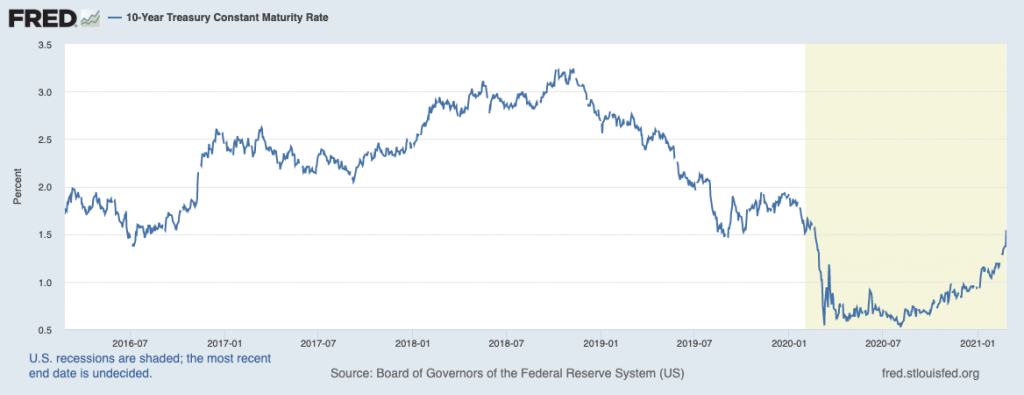

There’s no denying that we’ve seen a massive move in global bond yields recently. Having troughed at 0.5% in August, the benchmark 10 yr US Treasury yield finally broke above 1.5% this week before settling just below that level.

What’s the problem?

A 1.5% 10yr yield remains extraordinarily low in a historical context. And as Fed Chairman Powell explained last week, rising yields are a normal response to a recovering economy. That all sounds benign.

The factor that roiled markets was probably not so much the improvement in economic data. Rather, global bond investors are increasingly concerned about the timing of nearly $2 trillion in additional fiscal stimulus on top of the Fed’s ongoing monetary support. That combo, the argument goes, is a potent cocktail that will ignite inflation.

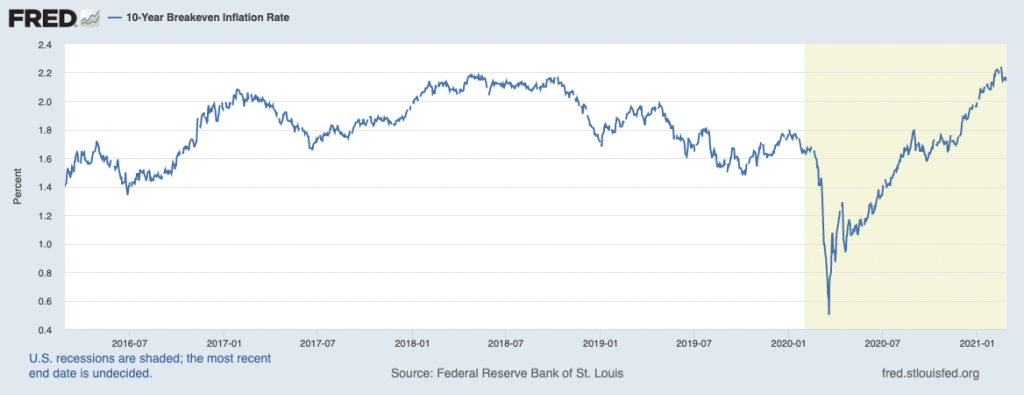

You can see the market’s concern reflected in the chart below of the 10-year breakeven inflation rate. This is the market-implied inflation rate over the next 10 years, derived by subtracting the yield of the 10-year TIPs from the 10-year Treasury.

For the record, I’m undecided whether inflation risks outweigh the risks of another threat of deflation. But that’s a topic beyond the scope of this post. And today, inflation has our attention. So how should we think about inflation in the context of multifamily investments?

Basic Real Estate Valuation

There are two primary drivers of returns to commercial real estate investors: the change in capitalization rate (the cap rate) and the change in net operating income (NOI).

Value = NOI / Cap Rate

Generally speaking, inflation alone doesn’t have a significant effect on real estate income expectations. Broad price inflation affects both the level of rents and operating costs, the components of NOI.

Because of this embedded hedge, inflation has minimal if any impact on cap rates. Therefore, it’s real yields that have historically affected cap rates more than nominal yields.

Contrast real estate to corporate bonds to see the importance of inflation protection. Since bonds provide fixed payments, inflation depresses the real value of those future fixed payments, making bonds sensitive to nominal yields.

Real Yields Matter More

Therefore, it’s not inflation or nominal yields that are the real problem. We need to watch carefully for a dramatic rise in real yields (nominal yields – inflation). Market expectations around changes to central bank policy would be the primary driver here.

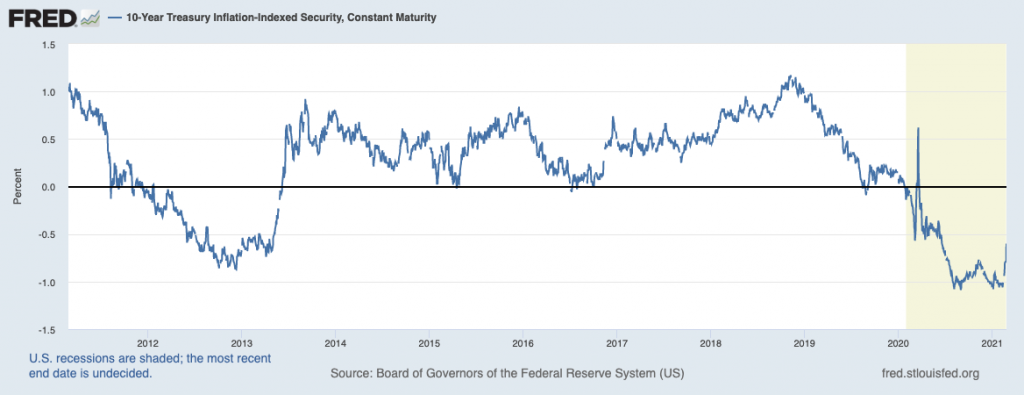

We’ve admittedly seen a recent increase in real yields, too (see the chart of US TIPS below). That said, the move from the bottom has been less dramatic. Also, the level of real rates remains negative, which is extraordinarily accommodative.

Reducing Risks Related to Rising Real Rates

Reasonable investors should expect real rates, and therefore cap rates, to rise from these extraordinarily low levels. There are a few ways to mitigate the risk.

- Return Expectations – as explained above, real estate returns come from changes in NOI and cap rates. The tailwind from declining cap rates has contributed to strong returns to real estate investors but cannot be relied upon. We always assume 50-100bps of cap rate reversion in our underwriting and rely on growth in NOI to drive our return expectations. For example, if similar assets trade at a 5 cap today, we might assume an exit at 5.5% in 5-7 years. We don’t know, nor can we control, what the market conditions will be in 5-7 years, but we certainly don’t want to rely on further cap rate compression to justify an investment.

- Buy Right – academic research supports the commonly held idea that real estate is a highly inefficient asset class. A property’s specific location and its future potential really matter, but we’re careful not to pay prices that already reflect that opportunity. Also, purchasing assets in attractive markets at prices substantially below replacement cost provides additional underlying support for valuation.

- Force Appreciation – investments can create value in attractive markets through renovation, repositioning, and improving operational performance. This strategy can reduce the potential negative impact of rising cap rates.

- Diversification – cap rates are driven by macro factors but also by changes in local conditions as well. A rapid change in a city’s economic outlook or tenant preference can dramatically impact cap rates. Therefore, spreading your exposure across multiple markets with attractive characteristics can provide some protection.

While far from exhaustive, I hope this offers some perspective on how inflation and changes in bond yields may affect multifamily assets. Click here to learn more about investing in cash-flowing real estate with Cove Investments.